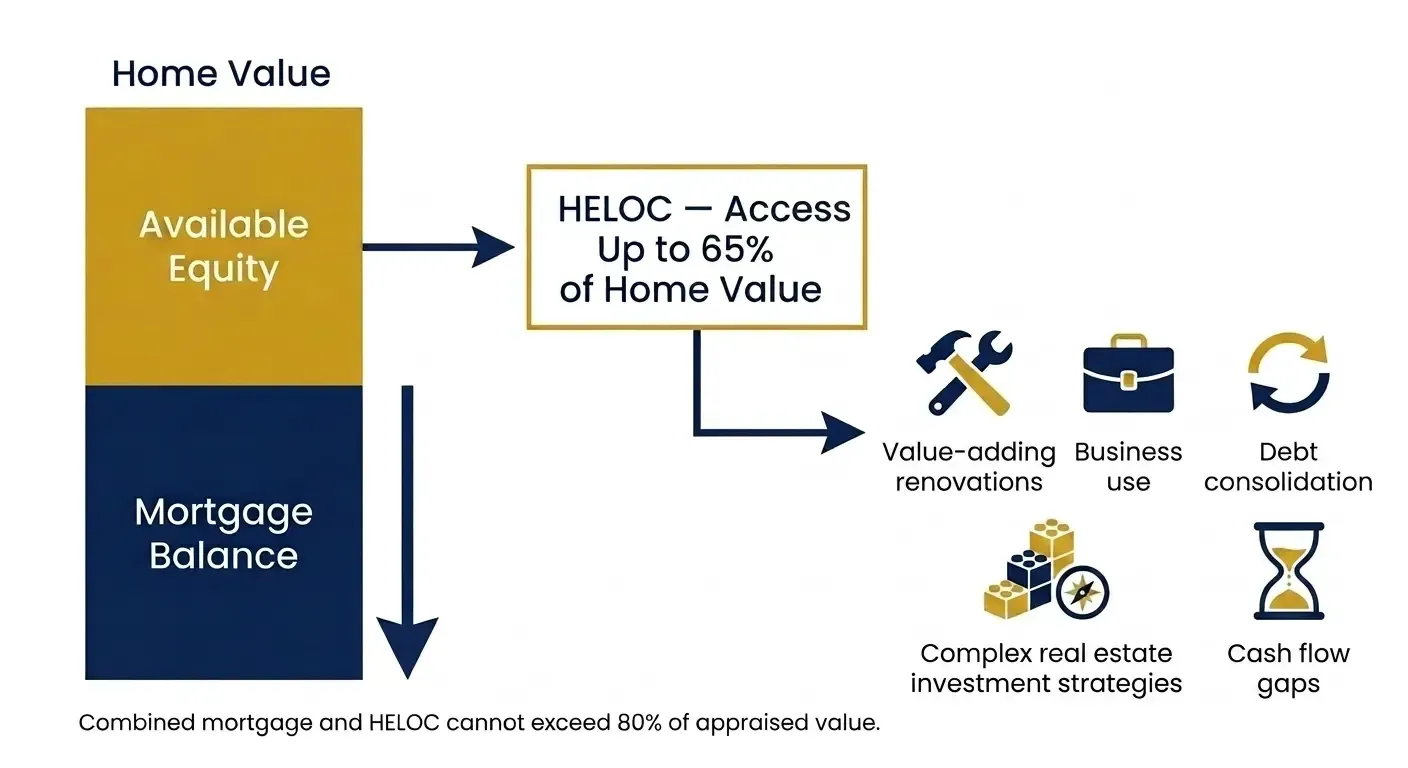

A Home Equity Line of Credit gives you access to the equity in your home on a revolving basis — you borrow what you need, when you need it, and pay interest only on what you use. It is the most flexible borrowing tool most homeowners have access to, and one of the most consistently misused.

A HELOC is secured against your home, which is why the rate is significantly lower than unsecured credit. Most lenders will advance up to 65% of your home's appraised value as a HELOC, with the combined mortgage and HELOC not exceeding 80% of the value. Accessing a HELOC requires either refinancing your existing mortgage or setting it up at purchase or renewal.

Used deliberately, a HELOC serves a range of legitimate financial purposes — value-adding renovations that improve the property itself, business use for self-employed borrowers managing variable income, debt consolidation at a significantly lower rate than unsecured credit, complex real estate investment strategies where equity in one property funds the next acquisition, and short-term cash flow bridging where timing gaps arise and a clear repayment plan is in place.

What a HELOC is not is a substitute for an emergency fund or a cash flow management tool. Interest-only payments mean the principal never moves unless you make it move. The flexibility that makes it valuable is the same flexibility that makes it easy to misuse.

A HELOC is particularly relevant in two situations that carry their own considerations: real estate investors using equity in an existing property to fund the next acquisition, and self-employed borrowers managing variable income or business cash flow alongside a mortgage obligation.